David@GAPInsurance

-

Posts

186 -

Joined

-

Last visited

Content Type

Profiles

Forums

Gallery

Shop

Events

Downloads

Everything posted by David@GAPInsurance

-

Skoda GAP insurance

David@GAPInsurance replied to Rutty555's topic in Skoda Octavia Mk III (2013 - 2020)

I look forward to hearing from you Jono. Whilst we're on the subject, some people assume that because Replacement GAP insurance refers to the cost of replacing the vehicle, it must be the case that a claim would involve the GAP insurer supplying a physical replacement vehicle. Whilst this may be the case for some policies, it's NOT the case for ours. Both our Invoice and Replacement GAP insurance policies involve (subject to any finance secured on the vehicle being cleared first) cash payouts to the policyholder who would then be free to use the funds they receive towards the cost of purchasing any vehicle from any dealership of their choice. dredge3, I guess it's not impossible that they agreed to reduce the cost of their Replacement GAP insurance policy to match their Invoice GAP insurance policy, but, you might want to double check what policy it is (particularly if you've/she's bought it already) because if it is Invoice GAP insurance, then it's not really about getting "a new car no matter when the claim is", in fact, in your case with a PCP neither policy type will be about specifically getting "a new car" (unless the finance has been cleared by the time of any claim). To clarify, what I mean is this... Some people assume that with a GAP insurance claim, they'll get to acquire a new vehicle and simply continue making the same monthly repayments on their existing finance agreement... this is not the case. If your invoice price was £27k, all things being equal, if you have an Invoice GAP insurance policy and at the time of a claim the settlement figure of your PCP agreement is less than £27k, the policy will be aiming to pay the difference between your Motor Insurance payout and £27k. Therefore all things being equal, the combined sum of the Motor and GAP insurance payouts should be £27k... however you'll have a sum of money that is due to the finance company to clear your liability to them as a priority. For the sake of example, lets say this is £17k. If this was the case, you'd be able to use the surplus funds (£10k) towards the cost of your next vehicle. Presumably, this would entail you taking out a new PCP agreement on the next vehicle and putting some or all of the £10k down as a deposit. Replacement GAP insurance is superior to Invoice GAP insurance when the cost of replacing the vehicle is more than the £27k you originally bought it for. Following on from the example above, if the replacement cost of a new equivalent vehicle was say £28.5k at the time of claim, the Replacement GAP insurance would aim to pay the difference between your Motor Insurance payout and the £28.5k replacement price, therefore after settling the finance (if we assume the same £17k settlement figure as above), you'd be left with £11,500 to put towards the cost of your next car. So you see... it's about the money you're left with (after clearing the finance) rather than about getting "a new car" per se. However, your wife is apparently under the impression that it's about getting a "new car no matter when the claim is". In the examples above I've assumed that the settlement figure of the finance agreement at the time of claim is LESS than the original invoice price (Invoice GAP insurance) and LESS than the replacement vehicle price (Replacement GAP insurance)... depending on the sums involved (the amount of deposit put down, negative equity brought forward from a previous vehicle, interest rate, finance duration), this may not always be the case and it's important for anyone else reading this thread generally, that they don't just make the assumption that "Replacement GAP insurance" = "Replacement Car" or even that it always equals "money towards a Replacement Car". What I mean is... Invoice GAP insurance Aims to pay the difference between your Motor Insurance payout and the greater of either: The amount outstanding on finance at the time of claim, OR The original invoice price that you bought the vehicle for. Therefore in the event that you financed the vehicle with little or no deposit, or brought forward negative equity from a previous vehicle (note that usually you have to pay an additional surcharge to specifically incorporate cover for Negative Equity on a previous vehicle, with a GAP insurance policy), or the agreement involves a particularly high interest rate and (particularly when combined with a high interest rate) a long finance agreement duration (or any combination of these), an early claim (when you've paid little of the finance off) *could* see you facing a settlement figure greater than the original invoice price... in which case the policy will be aiming to pay the difference between your Motor Insurance payout and the amount outstanding on finance, in which case granted you'll have (in theory) your finance agreement cleared, but you'll be left with no funds whatsoever to put towards your next vehicle (other than your own money). Similarly... Replacement GAP insurance Aims to pay the difference between your Motor Insurance payout and the greater of either: The amount outstanding on finance at the time of claim, OR The original invoice price that you bought the vehicle for, OR The cost of replacing the vehicle at the time of claim with one of the same Make, Model, Age, Specification and Mileage as your original vehicle was when you first bought it Therefore if, for example, you financed a brand new car, received no (or very little) discount, putting down little (or no) deposit or brought forward negative equity, or it's a high interest rate over a long duration etc etc, an early claim *could* see you facing a finance agreement settlement figure greater than even the replacement cost of the vehicle in which case all things being equal the policy will pay the difference between your Motor Insurance payout and the finance agreement settlement figure, granted leaving you with no finance liability, but also leaving you with no surplus funds whatsoever to put towards your next vehicle. dredge3 - it may be that none of this affects you, but as mentioned above, I wanted to clarify this for other browsers of this forum who might otherwise assume that GAP insurance is explicitly about getting a "new car" regardless. In a similar context, I should point out that whilst some/most companies do sell Invoice and Replacement GAP insurance that work as I've explained above (some of those companies referring to them as "Combined" policies), there are Invoice and Replacement GAP insurance policies out there that will leave you with a shortfall if the Finance Agreement settlement figure happens to be greater than the original invoice price (Invoice GAP insurance) or greater than the replacement vehicle price (Replacement GAP insurance). I hope this makes sense. Hi Paul, Yes, just mention that you're a BRISKODA forum member when you call. -

Skoda GAP insurance

David@GAPInsurance replied to Rutty555's topic in Skoda Octavia Mk III (2013 - 2020)

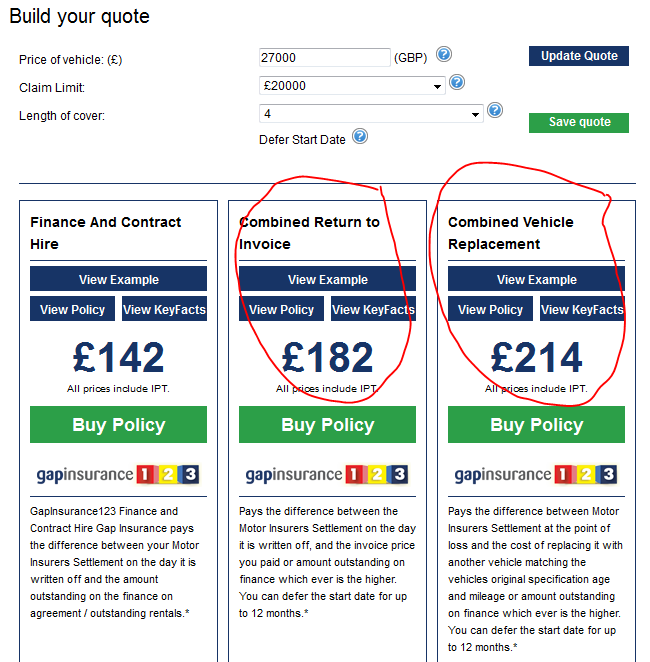

Are you sure you've understood that correctly? The Gap123 website quotes: £182 for their Invoice GAP insurance policy ("Pays the difference between the Motor Insurers Settlement on the day it is written off, and the invoice price you paid or amount outstanding on finance which ever is the higher") and £214 for their Replacement GAP insurance policy ("Pays the difference between Motor Insurers Settlement at the point of loss and the cost of replacing it with another vehicle matching the vehicles original specification age and mileage or amount outstanding on finance which ever is the higher"). I just took this screenshot (the red circles are my own doing :-)) Incidentally and by comparison, after your BRISKODA forum-member discount, our prices would be: Invoice GAP insurance, 4yr, £20k Claim Limit = £169.02 Replacement GAP insurance, 4yr, £20k Claim Limit = £194.05

-

Skoda GAP insurance

David@GAPInsurance replied to Rutty555's topic in Skoda Octavia Mk III (2013 - 2020)

I think perhaps one of us is entirely misunderstanding the other's point. If I buy a car for say £28k then it's declared a Total Loss very early in my ownership of it and it's value (according to say Glass's Guide) was say £24k. I would be expecting my Motor Insurer (assuming they're not replacing it New-For-Old) to be paying out in the region of £24k for it. They are afterall obliged to pay me a sum of money that would allow me to purchase a vehicle of the same age, mileage and condition as was applicable to my (now written-off) vehicle immediately prior to the incident that led to it being declared a write-off. If they found a reason to only pay out £22k for it, assuming I understand your logic correctly, you're saying that the £2k difference between my Motor Insurer's payout of £22k and the Glass' Guide Retail Value of my vehicle at £24k, is scary. My argument is that the £6k difference between my Motor Insurer's payout and the £28k original purchase price is, well, "scarier" :-) (In theory this £6k shortfall would be covered by an Invoice GAP insurance policy) If we use this same logic and go for a much later claim (i.e. I've owned the vehicle for a longer period of time)... The same car I bought for £28k is declared a Total Loss when it's worth say, £10k. I'd be expecting my Motor Insurer to be paying out circa £10k for it. If they found a reason to only pay £8k for it (again assuming I'm understanding your logic correctly), you're saying that the £2k difference between my Motor Insurer's payout and the £10k value of my car is scary. My argument is that the £20k difference between my Motor Insurer's payout of £8k and the £28k original purchase price is, well, considerably more scary than a £2k shortfall and scarier still is the prospect that to buy a brand new version of the same car again might well now be higher than the £28k I originally paid (The £20k difference theoretically being covered by an Invoice GAP insurance policy and any further increase in the brand new replacement cost theoretically being covered by a Replacement GAP insurance policy). Putting it another way, at any given time (with the exclusion of some finance agreements and most Contract Hire agreements) an early claim would involve (specifically in relation to any difference between the value of the car and the Motor Insurer's payout) relatively low figures because, regardless as to whether your car is worth £24k or £4k your Motor Insurer (short of a New-For-Old claim or Agreed Value policy) is only obliged to pay what your car is worth. Of course they'll try to low-ball you as we all know, but even so any difference between the value (either market driven or in reference to one or more industry guides) and what they actually pay out is not likely to be considerable. Ultimately though, this is a conversation about GAP insurance and you stated that the first year involved the biggest and scariest numbers, this IS incorrect from an Invoice or Replacement GAP insurance perspective because the numbers get bigger and more scary as time goes by (from the perspective that NOT having GAP insurance would see your potential financial shortfall increase as times goes by). If I've misunderstood your point, I apologise - though if I have, perhaps you could clarify your interpretation of the "difference between payout and value"? -

Skoda GAP insurance

David@GAPInsurance replied to Rutty555's topic in Skoda Octavia Mk III (2013 - 2020)

Out of interest... what was the invoice price of your car and what policy claim limit did you choose? -

Skoda GAP insurance

David@GAPInsurance replied to Rutty555's topic in Skoda Octavia Mk III (2013 - 2020)

nicowalker85 - according to other posts in this forum, you've ordered an Octavia SE-L (for the sake of this price comparison I'm assuming "hatch" and manual) with Silver Rails, Sunset Glass, Winter Pack and Smart Link. Looking this up online I got to a list price of £22,970 and couldn't quickly find prices for the Silver Rails, Winter Pack and Smart Link. Let's assume with everything in, the full list price was circa £24k (you may or may not have received discount off the full list price but that's irrelevant at this stage - unless the discount brought your purchase price down less than £15k (in which case our policies will be cheaper still)). Based on a vehicle bought for £24k, we'd be able to provide you with the following GAP insurance options: 3yr duration, £20k Claim Limit (you almost certainly wouldn't need this much, but many motor dealer policies have a £20k limit so I'm including this as a reference point - note that we can supply policies for up to 5-years ): Invoice GAP insurance = £110.25 less 10% forum discount = £99.22 Replacement GAP insurance = £161.78 less 10% forum discount = £145.60 Under no circumstances should £299 for a 3-year Invoice GAP insurance policy EVER be considered "worth the money". It's the dealer overcharging for it and hopefully, is a practice that will be curtailed when the new laws covering Motor Dealer's selling of GAP insurance come in to force on September 1st this year. Also, as I've said in earlier posts, never "forget the first year" (this is a dangerous game) unless you have thoroughly investigated your Car Insurance policy to determine: That it provides New-For-Old cover in the first year That their New-For-Old cover is actually any good (too many aren't) See here for more details. For clarity, with those prices above, you could purchase a policy for £99.22 and have it start immediately to cover years 1, 2, and 3. Or, if you have got New-For-Old cover from your Motor Insurance and (having checked) you're happy with it, you could purchase a policy for £99.22 and have the start date delayed so that it covers years 2, 3, and 4 at no additional cost. Or of course you could wait and buy the GAP insurance towards the end of the first year and perhaps then just for years 2 and 3 etc - although there may be some price changes over the next 12 months) You have plenty of options, but it's not something you should approach without due-consideration. (The prices quoted in this email are based on a vehicle purchased for £24k a 3yr policy duration and £20,000 Claim Limit. Valid for next 30-days.) -

Skoda GAP insurance

David@GAPInsurance replied to Rutty555's topic in Skoda Octavia Mk III (2013 - 2020)

Yes... our previous replies crossed... for clarity: We publish our claim data - so far as I know we're the only GAP insurance provider to do so. See either www.gapinsurance.co.uk/invoice-gap-insurance.asp or www.gapinsurance.co.uk/replacement-gap-insurance.asp (scroll to the bottom for each). -

Skoda GAP insurance

David@GAPInsurance replied to Rutty555's topic in Skoda Octavia Mk III (2013 - 2020)

If you were happy with the end price you got, that's good, but sadly you'll still have overpaid for it. There's still time to cancel within your cooling off period and buy a much cheaper (and superior) policy elsewhere. We publish our claim data - so far as I know we're the only GAP insurance provider to do so. See either www.gapinsurance.co.uk/invoice-gap-insurance.asp or www.gapinsurance.co.uk/replacement-gap-insurance.asp (scroll to the bottom for each). £500 for GAP insurance is insane For circa £500 we'd be looking to cover a vehicle bought for a sum in excess of £100k, with Replacement GAP insurance over 5 years! For our policies, aside from your contact details, in order to purchase a policy, we need to know: Vehicle Make Vehicle Model Vehicle Derivative (the specific version of that model) Invoice Price Date of First Registration Date of Delivery Funding Method Mileage Reading (normally just 1-2 for a new car) You *can* purchase in advance with estimated/anticipated info if you need to, (and then update later - at no cost) but we don't recommend doing so more than two-weeks prior to the expected delivery date. In any case, the purchase process only takes a few minutes from start to finish and the policy can be live and active etc immediately at the end of that process (unless you choose to delay the start date at all - e.g. if you have New-For-Old cover via your Motor Insurance for the first year, and you're happy with it, you might choose to delay the start date by up to 12 months from when the vehicle was first registered). We allow people to buy either Invoice or Replacement GAP insurance up to 12 months after taking delivery of their vehicle. As you point out, some Motor Insurance policies cover a brand new vehicle on a new-for-old basis during the first year so it's not always necessary to have GAP insurance in the first year... but... some New-For-Old schemes are very good and others are a waste of space. See here for things to look out for: http://blog.gapinsurance.co.uk/index.php/2015/02/23/the-perils-of-new-for-old-cover/ £299 is absurdly high still. Get a quote from us at www.gapinsurance.co.uk and remember that you'll pay 10% less (you'll need to buy over the phone to get the discount). The first year of GAP Insurance is often far from worthless due to the fact that (as I've said above) some Motor Insurance new-for-old schemes are, well, rubbish (see: http://blog.gapinsurance.co.uk/index.php/2015/02/23/the-perils-of-new-for-old-cover/). Incidentally, the logic that the first year is the "year when the numbers are biggest and scariest" is completely incorrect when it comes to Invoice or Replacement GAP insurance. To clarify, in the event of your vehicle being declared a Total Loss ("written off"): Our Invoice GAP insurance policy... Aims to pay the difference between your Motor Insurance payout and the greater of either: The original invoice price that you bought the vehicle for, OR The amount (if any) outstanding on finance at the time of claim Our Replacement GAP insurance policy... Aims to pay the difference between your Motor Insurance payout and the greater of either: The cost of replacing your vehicle with one of the same Make, Model, Specification, Age and Mileage (or nearest equivalent) as your original vehicle was at the time you first bought it, OR The original invoice price that you bought the vehicle for, OR The amount (if any) outstanding on finance at the time of claim Thus, the "gap" gets larger as time goes by therefore the numbers are technically at their "biggest and scariest" at the very end of the policy (we provide cover for up to 5-years) when the current value of your vehicle has depreciated furthest from its original purchase price. I hope that all makes sense and if anyone has any further questions about GAP insurance I'd be very happy to help. Best wishes David -

Skoda GAP insurance

David@GAPInsurance replied to Rutty555's topic in Skoda Octavia Mk III (2013 - 2020)

Shameless plug... we sponsor this forum and forum members get 10% discount off our full prices! See www.gapinsurance.co.uk :-) -

We're now able to provide Invoice or Replacement GAP insurance for a vehicle that you purchased up to ONE YEAR ago (previously six months)? We've also revised our Replacement GAP insurance policy so that it's now a combination of Finance, Invoice and Replacement GAP insurance which means that in the event of your vehicle being written off through accident, fire or theft, the policy will pay the difference between your Motor Insurance payout and the greater of either: The amount outstanding on finance (if any) at the time of claim, OR The original Invoice Price that you bought the vehicle for, OR The cost (at the time of claim) of replacing your vehicle with one of the same Make, Model, Specification, Age and Mileage as your original vehicle was at the time you first bought it. In a further improvement, we're now able to cover vehicles bought for up to £150,000 and provide Claim Limits (subject to the vehicle value) of up to £100,000. If you bought a car more than 6-months ago and have since been excluded from buying either Invoice or Replacement GAP insurance, now is your chance. Get a quote online at GapInsurance.co.uk or call us on 01943 850999 for more details.

-

Recommended GAP insurance

David@GAPInsurance replied to johnthesparky's topic in Skoda Octavia Mk III (2013 - 2020)

You're very welcome! Thank you for your custom :-) -

Recommended GAP insurance

David@GAPInsurance replied to johnthesparky's topic in Skoda Octavia Mk III (2013 - 2020)

I've been out of the office all day today. Did you manage to speak to one of the team and is everything sorted for you now? If it's a Contract Hire Agreement, you WILL NOT qualify for the 1st year "replacement cover" from your Motor insurer (aka "New-For-Old cover"). This is because in order to qualify for New-For-Old cover you have to the be the first registered keeper of the vehicle and in the case of a Contract Hire Agreement you are NEVER the registered keeper of the vehicle (the finance company remain the entity named on the V5 Registration Document at all times). You can also NOT have our Replacement GAP insurance policy. Specifically you need a Contract Hire GAP insurance policy. However, we've taken the slightly confusing step of merging Contract Hire GAP and Invoice GAP insurance together in to one document. It basically results in a policy that works one way if you're buying the vehicle (paying the difference between motor insurance payout and original invoice price) and another way if you're Contract Hiring the vehicle (paying the difference between your Motor Insurance payout and the settlement figure of the Contract Hire Agreement at the time of loss - if there is one! As for what to look for and what questions to ask, we can approach this two ways.. 1. Phone them. You specifically want to know how, technically, they will calculate your liability in the event of a Total Loss. 2. Scan and email a copy of your Contract Hire agreement to me (I don't need to see any data personal to you... just the sections of the contract discussing Loss or Damage to the vehicle) I can then give you my views on it. As for keeping the price rock-bottom, in order to give you a quote, I'd need to know the following: The invoice value of the vehicle (the p11d value if you have it) The structure of your monthly rentals... e.g. is it 3 + 35, or 6 + 35 etc? The value of your monthly rentals Whether the monthly rentals include Maintenance and if so, how much is the maintenance element. Whether this is a personal or commercial lease and if you're registered for VAT The annual mileage limit of the Contract Hire agreement That's one approach and many people do it, particularly as GAP insurance for Contract Hire Agreements really isn't (when you're not dealing with a motor dealer and/or finance broker) that expensive in the grand scheme of things. However it's still not worth spending the money if it's very clear that you don't need it. I speak from experience too... my old car (Volvo V40) was written off as a result of an accident in December 2014. The finance house (Volvo Car Finance (Lex)) calculated that the remaining balance of the Contract Hire Agreement was £18,305 (a combination of the outstanding monthly rentals and what they thought the car was worth). My motor insurance paid out £15,000 (£14,900 after deducting my £100 excess) directly to the finance house and normally you'd expect that they'd have come after me for the remaining. Except they didn't, plus not only did I get to walk away with nothing else left to pay, but they also refunded the two monthly rentals that I'd paid in the period of time it took the Motor Insurer to finalise the claim and pay out. Clearly GAP insurance for such a Contract Hire Agreement would have been utterly pointless. But it was quite apparent within the Contract Wordings that it wasn't necessary, sadly not all Contract Hire Agreements are so clear cut and in fact some are (IMO) intentionally unclear. My advice would be, "If there's any doubt, buy GAP". Best wishes David -

Recommended GAP insurance

David@GAPInsurance replied to johnthesparky's topic in Skoda Octavia Mk III (2013 - 2020)

I'm afraid I don't have time to go in to this in too much detail right now (I'm just getting ready for a fundraising event this evening for a football team that I play for) but if you look here: http://www.briskoda.net/forums/topic/332184-gap-insurance/page-2 (I think it's about the 25th post/comment on that page, from me) I give some advice about Contract Hire Agreements and how actually you may not need GAP insurance at all - it all depends on the wording of your Contract Hire Agreement. I apologise for any typos in this message, I'm typing quickly on an iPhone and the productive text is a killer! Cheers David -

Recommended GAP insurance

David@GAPInsurance replied to johnthesparky's topic in Skoda Octavia Mk III (2013 - 2020)

You mention New-For-Old but then appear to specify "return to invoice" - if you have an RTI policy (we call it "Invoice GAP Insurance") it isn't New-For-Old cover. You'd need Replacement GAP insurance for that. Or... is it that you're relying on your Motor Insurer's New-For-Old cover in the first year and then RTI cover in the 2nd, 3rd, 4th and 5th year? Out of interest too... what was the invoice price of your vehicle (the actual On-The-Road (cash) price) and how did this compare (assuming you bought it brand new) to the manufacturer's full list price? I've just replied Kevin - cheers. -

Recommended GAP insurance

David@GAPInsurance replied to johnthesparky's topic in Skoda Octavia Mk III (2013 - 2020)

Only just stumbled across this post... just to second what others have already said... I am www.gapinsurance.co.uk and forum members get 10% discount. I'm happy to answer any questions whatsoever about GAP insurance, whether you buy from us or not. Give me a shout if you need anything. Best wishes David -

I'm sorry Steve - somehow I missed he notification of your reply in this thread. To be honest, based on what you've posted your Motor Insurance wording doesn't look too bad. The above is pretty standard stuff. However it would be useful to know what they would constitute (in terms of the cost of a repair) as "beyond economical repair". For example below, they go on to say the bit I've highlighted red. Ideally, what you would NOT want, is them being able to declare the vehicle beyond economical repair if say, the cost of repair equated to more than 50% of the Market Value of the vehicle whilst they only entertain giving you a new-for-old replacement if the cost of repair exceeded 60% of Market Value - that 10% difference (assuming it exists) could come back and bite you (assuming you'd delayed the start date of a GAP insurance policy). The only thing they don't seem to say above, is what happens if you DO qualify for a New-For-Old replacement vehicle but, they cannot source one at the time of claim. Some will only pay you the Market Value of your car (you'd need GAP insurance), some will pay you back the original purchase price (you *may* not need GAP insurance) and others will pay you the full manufacturer's list price of the brand new vehicle and leave you to source your own (you probably wouldn't need GAP insurance). Without it being explicitly defined in their wordings, my assumption would be that they'd revert to a Market Value payout, but it may be worth pushing them for an answer (if you haven't already). Not necessarily. Motor Insurance policies that include a New-For-Old feature, cover a brand new vehicle on a New-For-Old basis so long as at the time of claim you were (and still are) the first and only registered keeper, the vehicle is still less than 12 months old, any finance company agrees (what company wouldn't agree to getting a newer vehicle back than they originally anticipated?) and that the cost of repair exceeds whatever threshold they set down. This of course means that it doesn't matter when you bought the policy in terms of the age of the car... e.g. if you bought your policy after having already owned the vehicle for 11 months, but a write-off occurred just before it turned 1yr old, if that motor insurance policy included New-For-Old cover and you met the qualifying criteria it'd be handled accordingly. Thus, all it ties you to (assuming you went down the route of delaying a GAP insurance policy start date) is to ensure that whatever new policy you take out also incorporates New-For-Old cover for a vehicle that you bought brand new. However even that isn't set in stone... If you bought a policy from us and delayed the start date until March 14th next year, at any time before that policy starts you can elect (free of charge) to amend the policy start date and have it start sooner if you require. Equally within the first 30-days the opposite is true. Buy a policy and have it start on March 14th this year and you get a 30-day cooling off period during which (assuming no claim has been made) you can make virtually any change to the policy and if you came back to us before April 14th having found a Motor Insurance policy that provides New-For-Old cover that you're satisfied with, you could elect (again free of charge) to revise the policy start and end dates so that it becomes a deferred policy. To be fair you could do the latter any time within the first 6-months, it's just that after the first 30-days you'd lose some of what you'd paid for the policy first time around on a monthly-pro-rata basis. Ok, so... the type of policy you refer to is our Replacement GAP insurance policy which, in the case of a vehicle you bought brand new (1st keeper etc) and that vehicle being declared a Total Loss (written off) within the policy term will pay the difference between your Motor Insurance payout and what it would cost to replace the vehicle with a brand new version of the same (or nearest equivalent) vehicle at the time of claim - even if that replacement vehicle costs more than you bought the vehicle for first time around. In addition there's an Invoice GAP insurance safety net meaning that in the unlikely event that the replacement vehicle at the time of claim on sale for less than what you bought the vehicle for first time around, the policy will revert to Invoice GAP insurance and pay the difference between your Motor Insurance payout and the original purchase price you bought the car for. Prices: Prices vary depending on the policy type, duration and claim limit. I've listed the variations below as examples, but note that other claim limits (etc) are available. 3yr Replacement GAP insurance, £17,500 Claim Limit = £150.78 less 10% discount comes to £135.70 3yr Replacement GAP insurance, £20,000 Claim Limit = £161.78 less 10% discount comes to £145.60 4yr Replacement GAP insurance, £17,500 Claim Limit = £186.10 less 10% discount comes to £167.49 4yr Replacement GAP insurance, £20,000 Claim Limit = £193.10 less 10% discount comes to £173.79 Further note that these prices are for the specified duration and (as mentioned above) that it's a no-cost option to defer the start date by up to a year from first registration so, for example, a 3yr policy at £145.60 could be for a policy running for years 1, 2 and 3 OR years 2, 3, and 4. Conversely, the four year policies can be for years 1, 2, 3 and 4 OR years 2, 3, 4 and 5. Any further questions, just ask. Cheers David

-

Dealer's make a HUGE amount of profit on GAP insurance alone. The FCA's Market Study in March 2013 stated that they were overcharging UK consumers by circa £76m per year in the process! But as I said above, don't bank on it. Some New-For-Old schemes from Motor Insurer's are really poor. It will pay to carefully check the terms of your Motor Insurance policy and you should read this for guidance. In any case, if you are inclined to buy GAP insurance, you should NOT rely on the New-For-Old cover in the first year and delay buying GAP insurance until the end of year one. This is because if you wait more than 6-months from taking ownership of the vehicle to buy GAP Insurance the cover-level you can get then is drastically reduced compared to the cover level you can buy within the first 6-months. That's great in terms of increasing your own ability to avoid an accident, but is of limited use if someone else causes the accident or, if a thief decides to relieve you of your vehicle. GAP Insurance is not just about accidents, it covers in the event of a Total Loss through accident, fire or theft.

-

Hi Mike, So, assuming the car is brand new and you are to be the very first registered keeper, you can indeed get the type of GAP insurance that you describe. It's called Replacement GAP insurance. You can read more about it here. You can view our policy terms and conditions here. In a nutshell though... if you bought your car brand new and took out Replacement GAP insurance, in the event of that vehicle being declared a Total Loss (written off) within the policy duration, the policy will pay the difference between your Motor Insurance payout and what it would cost at the time of claim to replace the vehicle with a brand new version of the same (or nearest equivalent) vehicle at that time - even if the replacement vehicle costs more than you bought the car for first time around. In the event that you'd financed the car and there was an outstanding balance due to the finance company at the time of loss, you'd clearly then use the combined sum of your Car and GAP insurance payouts to clear some or all of the remaining finance and any surplus funds would then be yours to use against the cost of any vehicle from any dealership of your choice. Of course, if you had not financed the car (or you had cleared the finance by the time of loss) all of the funds would be yours to use against the cost of your next car. You don't mention what duration policy you'd require nor whether the ~£11k is the price after any discount, but based on a vehicle purchase price of £11k as an indication of cost, we could provide you with a 3yr policy incorporating a £10k Claim Limit for a one-off all-inclusive fee of £99.66 and as a BRISKODA forum member you'd get a further 10% discount bringing it down to £89.69. (Other durations and Claim Limits are available). Note that in some cases, it's possible that your Motor Insurance policy may cover you on a New-For-Old basis in the first year already. If it's a decent cover level (the quality of New-For-Old schemes vary considerably from one insurer to another) it could mean that you don't actually require GAP Insurance in the first year. In which case, you'd still need to buy GAP insurance within 6-months of taking ownership of the vehicle, but, when you bought it you could specify when you wanted the policy to start and you could choose a start date up to 12 months ahead of when the vehicle was first registered - thereby avoiding duplicate cover in the first year but still benefiting from GAP insurance in the latter years. What's more is that this is a no-cost option, in which case you end up with a 3yr policy covering you for years 2, 3, 4 (without the additional expense of paying for a 4-year policy) or you could save a little money upfront by buying a 2-year policy that ends up covering years 2 and 3 only. However, some New-For-Old schemes are, frankly, rubbish (the criteria you're required to meet in order to qualify for a new car replacement being so difficult to meet that the policy may as well not have New-For-Old cover), so it's clearly important to check out your Motor Insurance policy in detail and verify whether or not it would be prudent to have GAP insurance in the first year or not. Please see this article here, for guidance on what to look for. If I can be of any further assistance, please don't hesitate to ask Best wishes David

-

I've got relatives on Manchester road in Woolston. Small world! Their house backs on to a school playing field (or at least it did - I've not been there for quite a while) and I'd spend ages playing on the field whenever I was there. One time (maybe around 11/12yrs old) I was approached by another lad who asked me if I'd be his girlfriend... confused, I pointed out that I was male... he made his excuses and left pretty sharpish... and I went straight inside to my Mum and demanded that I wanted my (then rather long as I wanted to look like a "surfer-dude") hair cutting as soon as possible :-) My dad dined out on that, at my expense, for years. Glad to hear that Mr Smiths has been saved! Let me know what your Motor Insurer says and if you get any strange answer(s) give me a shout. Indeed, although it's not worth paying any extra if you're not likely to need GAP insurance at all :-) I look forward to seeing your docs and advising accordingly. Best wishes David

-

Incidentally Steve, what part of Warrington are you at? I basically grew up in Warrington... initially in Callands but then Orford followed by Culcheth (my parents had a pub there) and then Birchwood. My parents had one of the pubs in the Town Centre for a while too: Time Square (although it changed it's name to Bar Tempo when they initially took it over). Was gutted to hear recently that Mr Smiths is going to become apartments... I lost many nights in that place! :-)

-

Sorry for the delay people... March 1st and all that, things are pretty hectic right now :-) Ok, So... you've touched on a few things here... let's start with the easy one first... New-For-Old cover via your Motor Insurance New-For-Old cover from your motor insurer, does not apply to a leased vehicle. This is because, in order to qualify for New-For-Old cover, it will be a requirement that at the time of any Total Loss claim, you must have been and still be the first and only registered keeper of the vehicle (E.g. your details appear on the V5 DVLA registration document). In the case of a leased vehicle, it's the finance company that remains as the Registered Keeper of the vehicle (on the V5 document), they just happen to permit you to use it. What type of GAP insurance for a Contract Hire (Leased) vehicle? Specifically, you'd consider a Contract Hire GAP insurance policy, which (just like Finance GAP insurance policies of old) would, in the event of a Total Loss claim, pay the difference between your Motor Insurance payout and the settlement figure of the Contract Hire Agreement - the goal being to allow you to walk away at a "zero" position (no car, but no outstanding finance to settle before you can contemplate a new vehicle). In an effort to keep things simple (although arguably confusing matters too), we've chosen to have one single policy which is Finance, Invoice and Contract Hire GAP insurance in one document (our "Invoice GAP insurance policy"). In simple terms, the policy wordings explain that if you're buying the vehicle it's either Finance or Invoice GAP insurance (depending on the best payout for the policyholder at the time of claim) or, if your vehicle is the subject of a Contract Hire Agreement, it becomes Contract Hire GAP insurance. Do you need GAP Insurance for a Contract Hire (Leased) vehicle? It's an absurdly popular misconception that if you're leasing a vehicle you absolutely need to have GAP insurance. It's simply not the case. Consider.... I was involved in an accident on December 4th last year in my leased vehicle. My vehicle (along with two others) were written off as a result. The finance company told me that the combination of what they believed my vehicle was worth and the outstanding rentals that I was liable for, equated to around something like £18,300. My Motor Insurance company (correctly I should add) valued my vehicle at £15,000 but paid out only £14,900 due to a £100 excess on my policy. Most people would therefore assume that I was going to have a shortfall to pay (without GAP insurance) of £3,400 however, the finance company invoiced me for £100 (the excess that was deducted). This was because the terms of the Lease stated that they'd take the payout from my Motor Insurer as full settlement. They even went on to refund me the two monthly rentals I'd paid since the accident over the time it took for the Motor Insurer to payout. In very basic terms, if you have a Contract Hire agreement and your vehicle is declared a Total Loss before it ends, the Motor Insurer will pay the finance company what they believe the car to be worth and then there are three possible scenarios: The finance company holds you liable for the entire balance of outstanding rentals at the time of loss. This may or may not include a shortfall between what the Motor Insurer paid out and what the finance company believe the car to be worth. The finance company holds you liable for some (it could be a percentage of the entire sum outstanding or a cash value per monthly rental - I spoke to someone not too long ago who'd only have to pay £15 per monthly rental outstanding). The finance company (upon receipt of the Motor Insurer's payout) releases you of any further liability to them and allow you to walk away within nothing further to pay. Clearly No.1 above is the worst case scenario. Particularly if the Total Loss occurred within say, a few weeks of you taking delivery of the vehicle. You'd be pretty miffed if you'd leased the car over 3 years only to have the vehicle written off in the first month and then have the finance company come after you for three years of monthly rentals . Obviously No.3 is the best case scenario. You'd want GAP insurance in place if your lease agreement was somewhere between 1 & 2 above. You clearly wouldn't need GAP insurance if your lease agreement was the equivalent of 3 above. If you're not sure and have access to a scanner, I'd be happy to have you scan and send me a copy of your lease and I can let you have my interpretation of it. Give me a shout if you'd like me to do this for you. If you'd like me to provide you with a quote for GAP insurance on your vehicle, I'd need to know: The vehicle value (what would if have cost you if you'd bought it?) The structure of your agreement (How many rentals upfront followed by how many monthly rentals) How much your monthly rentals are The annual mileage limit of your lease agreement. Cheers David Firstly, in terms of your Motor Insurance providing New-For-Old cover in the first year, assuming you haven't already, please read this: The Perils Of New-For-Old Cover - New for Old schemes are not always what they seem to be. Secondly, you don't need to buy GAP insurance at the time you take delivery of the car. Your dealer will tell you that because they want you to buy their policy before you discover that you can buy superior cover at a lower price from from an independent provider such as us. We (and others) permit you to buy GAP insurance within up to 180 days (6-months) of taking ownership of the vehicle. So... assuming you have New-For-Old cover with your Motor Insurer and after researching how good it is (see the article above), it all stacks up and you're comfortable with the cover-level it provides in the first year, in theory you could wait up to 6-months from taking ownership of the vehicle to buy a policy and then at the time of buying it, elect to delay the start date of the policy by up to 12 months from when the vehicle was first registered. Meaning that yes, you could buy a 3-year policy, covering you only for years 2, 3 and 4 (in terms of the age of the vehicle). In terms of the cover-type... if you bought an Invoice GAP insurance policy (which is almost certainly the type of policy being (or that will be) offered to you by your dealer - even if they do refer to it as Vehicle Replacement Insurance), in the event of a claim, it will only be aiming to get you back up to the original £22,500 OTR price that you bought the vehicle for first time around. The policy you require in order to cover you up to the manufacturer's list price for buying a brand new version of the same (or nearest equivalent) vehicle at the time of claim, is Replacement GAP insurance. However this is a policy that pays out in cash and subject to if/when a claim happens, there'd be finance left to clear. So, for clarity, if your car was written off, your Motor Insurance pay out what they believe the car to be worth, we top that up (subject to the policy claim limit) to the cost of the manufacturer's list price for a brand new version of the same (or nearest equivalent) vehicle at the time of claim. The combined sum is used to settle any remaining finance secured on the vehicle (in practice it's likely the finance company will insist they get paid first and you only receive the surplus funds) and then you'd dispose of the funds as you saw fit... e.g. you can buy any vehicle from any dealership of your choice (we make no stipulation as to what you need to buy or from where). If your vehicle has a current list price of £26,530 and a final residual/balloon value of £10,000 at the end of the four year PCP agreement, I'd suggest that whether you go with 3-year (deferred by 1) or a 4-year policy, you should be looking at a policy Claim Limit of £17,500 or higher, though ideally at least £20,000. The reason is that, one way to look at the PCP agreement is that the finance house is suggesting that the car may drop in value from today's list price by up to £16,500. Our own claim statistics however show that the average vehicle will drop in value by between 50% and 70% over a three year period, which with a list price of £26,500 today would equate to a potential depreciation range of between £13,250 and £18,550. Consequently £17,500 as a Claim Limit appears a reasonable choice, however, this is just looking at by how much the car might drop in value from today's list price. It's not giving any consideration to the fact that the list price at the time of claim (e.g.if you had a claim in the last few days of the four year policy) could be greater than £26,500... £17,500 as a claim limit therefore begins to look a little ambitious. However it makes comparatively little difference to the cost of the policy, to give you an idea, based on a car purchased for £22,500 and after applying your 10% forum discount, the following prices would apply: 3yr Replacement GAP insurance £17,500 Claim Limit = £135.70 £20,000 Claim Limit = £145.60 £22,500 Claim Limit = £162.94* 4yr Replacement GAP insurance £17,500 Claim Limit = £167.49 £20,000 Claim Limit = £173.79 £22,500 Claim Limit = £210.11* * - Note that with this option, the policy Claim Limit matches the original OTR of the vehicle. Coming back to the issue of New-For-Old cover... If you consider the prices above, the cost of the 4yr £20k policy for example, is just £28.19 more expensive than the 3yr equivalent... you can spend the time researching the intricacies of your Motor Insurance policy and fighting with them to get a clear answer, or you could pay £28,19 extra and have the cover in place regardless. I hope this helps. Best wishes David

-

That's great news Alan, thank you! I hope she looked after you well... I taught her everything she knows :-P Not long until you get the car now! Thank you to you too tasmanuk - it was a pleasure to talk to you earlier. Regards David

-

Hello John, Firstly, I'm assuming that by "used" you're referring to a vehicle that was (or will be) more than 6-months old at the time you bought/buy it and the advice that follows is based on that. You're correct that used vehicles depreciate at a slower rate than brand new vehicles, but unless you've got a classic car, a used vehicle will still depreciate in value. Consider... whether your car is new or used, the "gap" between what your car is worth on any given day (its Market Value) and the original purchase price, continues to increase the more time that goes by. If your car is declared a Total Loss (written off) through accident, fire or theft, your Motor Insurer is only obliged to pay you the Market Value of your vehicle at the time of loss. With a vehicle bought on finance, depending on the exact structure of the purchase (the type and length of the finance agreement, the interest rate, the amount borrowed etc) and when the Total Loss occurred, it's possible in some circumstances that the finance agreement settlement figure could not only be greater than the amount paid out by your Motor Insurance policy but also in extreme circumstances (e.g. a very early claim), greater than the original invoice price of the vehicle itself. There are some exceptions, but generally speaking, there are two forms of GAP insurance that a Motor Dealer would offer you for a used vehicle bought on finance: Finance GAP insurance: Pays the difference between your Motor Insurance payout and the amount outstanding on finance at the time of loss. In theory, it will allow you to walk away in a "zero" position, e.g. no car but no finance either. However sooner or later, there'll come a time when you've paid off so much of the finance agreement that the Motor Insurer payout alone will be sufficient enough to settle the finance on its own, in which case the GAP insurance is then useless. There's a popular misconception that if you're buying a car on finance, you must have Finance GAP insurance, when in fact, in almost all (non-Contract-Hire) cases, Finance GAP insurance is a terrible form of GAP insurance and consequently, with the exception of some Motor Dealers that still peddle it, most (but not all) independent companies have stopped selling it as a standalone product. Invoice GAP insurance: Pays the difference between your Motor Insurance payout and the original purchase price of the vehicle. In most cases a payout on an Invoice GAP insurance policy will allow you to clear any remaining finance AND have money left over that you can then put towards your next vehicle - on this point it's worth noting that the "better" policies will payout in cash to the policyholder (that is to say, any surplus funds after settling any finance agreement (if any) secured on the vehicle) and not insist that the GAP insurer has to get involved in the supply of the vehicle or (as is sometimes the case) that you must go to specific dealer of their choice to organise your next vehicle. The problem with "traditional" Invoice GAP insurance however (specifically if there's finance involved) is that if you put little or no deposit down and the finance involves a particularly high interest rate, a very early claim can see the finance agreement settlement figure be a sum that is higher than the original purchase price of the vehicle. If this were to happen a "traditional" Invoice GAP insurance policy would only aim to get you back to the original vehicle purchase price and you'd still have to put your hand in your pocket to settle the remaining balance outstanding on finance. Combined Invoice/Finance GAP insurance: Recognising that Finance GAP insurance doesn't really cut the mustard and that "traditional" Invoice GAP insurance may still fall short for some finance vehicles, most companies have now moved to a policy that is a combination of both Invoice and Finance GAP insurance. In the event of a claim for a vehicle which is the subject of a finance agreement, there are two possible scenarios: The finance agreement settlement figure is MORE than the original invoice price of the vehicle. If this happens the policy becomes a Finance GAP insurance policy paying the difference between your Motor Insurance payout and the amount outstanding on finance at the time of claim. The aim being to allow you to walk away at a "zero" position. The finance agreement settlement figure is LESS than the original invoice price of the vehicle (or the finance has already been repaid). If this happens the policy becomes an Invoice GAP insurance policy paying the difference between your Motor insurance payout and the original invoice price of your vehicle. The aim being to allow you to clear any remaining finance AND have money left over that you can use against the cost of a new vehicle. So... that's the long answer... The short answer? With very few exceptions, every vehicle less than 10years old (cars have to be less than 10yrs old to buy GAP insurance) will depreciate and consequently I believe it's absolutely worth buying GAP insurance regardless as to whether your car is new or used - though you may not need as much cover (e.g. the Claim Limit) for a used vehicle as you would with a brand new vehicle. Then again I sell GAP insurance for a living, so perhaps I'm always going to say that How long after purchasing the vehicle do you have to purchase GAP insurance? Some Motor Dealers will tell you that you must buy GAP insurance on the day you buy the vehicle and then when you decline, they'll phone you a few days later to offer you the option to buy GAP insurance again . In contrast (though it does vary from one to another) independent providers will currently allow you up to 180 days (six months) to purchase an Invoice GAP insurance policy, and then after 180 days some providers will be only be able to provide you with an "Agreed Value GAP insurance" policy which, rather than securing the price you bought the car for, is at it's most basic level, about the value of your vehicle at the time you bought the policy. Obviously what I've posted above is quite general. If you'd care to share the details of your specific purchase with me either here on this thread or via PM, I can advise you specifically according to your own figures. No obligation and no pressure. I'm happy to help (as I'm sure other members of this forum will confirm). Regards David

-

I've just replied. Sorry for the delay. Alan, You are quite right... with your policy as it is, it's possible that your car could be written off and if one of the same (or nearest equivalent) vehicles was not available to your Motor Insurer, they'd only be paying you the Market Value of your vehicle which, assuming you'd delayed the GAP insurance start date by a year from first registration, would leave you in a position of having no GAP insurance. There's another issue too though (I've highlighted it green) in that even if a vehicle was available to them, the cost of the repair would have to exceed 60% of the manufacturer's list price of that replacement vehicle before they'd entertain supplying a physical vehicle to you... in which case, you have to know what their lower threshold is in terms of declaring the vehicle to be a Total Loss in the first place. For example, If you bought your car for £25,000 and it was involved in an accident at say, 11-months old, it's not unreasonable to say that it may have depreciated by £5,000 (if not more) by then... but with your car worth circa £20k, it would be somewhat normal for a Motor Insurer to declare the vehicle to be a Total Loss (write it off) if the cost of repair came to 50-60% of what your car was worth (this'd be £10k-£12k). However with your policy, Churchill are only going to provide you with a New-For-Old replacement vehicle (assuming they can get one) if the cost of repair exceeds 60% of the manufacturer's list price for the equivalent vehicle at the time of claim... this'd mean that the cost of the repair would have to exceed £15,000 in this example and that's assuming that the list price was still £25,000 at the time of claim and had not increased! Personally... in your position with your existing Motor Insurance policy, I would not be considering delaying the start date of a GAP insurance policy. I'd either have it starting on day one, or, I'd be looking to change Motor Insurance provider/policy to one that offers a superior New-For-Old scheme. As it happens, earlier today I published this blog article: The Perils Of New-For-Old Cover - it might be worth having a read. Best wishes David

-

Hello Alan Sorry for the delay. Firstly, your P/X value is basically your money. They bought your car off you for £X and you put that same £X towards the cost of the new car. It's not treated as discount, it's part of the money you spent. So, for a nice simple example if you bought the car for £23,000 less a PX allowance of £7,000, you still bought the car for £23,000! Secondly the interest rate is a side-issue with Replacement GAP insurance as this policy is not specifically interested in the Finance Agreement secured on the vehicle, other than to know who needs to be paid first (E.g. the finance company get their bit before you see anything - just as they would with your Motor Insurance payout - however, in this case, if you've only financed £16,000 of a £23k car, your Motor Insurance payout is likely to be sufficient to clear the finance at any given time.) Where a Finance Agreement (secured on the vehicle) of any nature is involved, the policy works as follows: Motor insurance pays out what they believe the car to be worth (this either is, or isn't sufficient to clear the remaining balance of the finance agreement at the time of loss. If it is sufficient, any surplus funds to come to you) Replacement GAP insurance pays the difference between your Motor Insurance payout and (in the case of a vehicle bought brand new for which you are the very first registered keeper) the manufacturer's list price at the time of claim for a brand new version of the same or nearest equivalent vehicle - even if that replacement vehicle costs more than you bought it for first-time around (subject to the policy Claim Limit). If your Motor Insurance payout wasn't enough to clear any outstanding finance in step 1 above, some of the GAP insurance payout will go to the finance company to clear your remaining liability to them and any surplus funds come to you. Of course if the finance has already been cleared, the whole GAP insurance payout comes to you. You then use the funds that you're left with towards the cost of any vehicle from any dealership of your choice. Using your figures in the event that your car is written off on day one, the Market Value of your 1-day old car (as paid out by your Motor Insurer) shouldn't be too far (if at all) different from the Manufacturer's List price for a brand new vehicle. In which case with such an early claim it's unlikely a claim would be required of a Replacement GAP insurance policy - or at least a minimal one only. Example... Not too long ago I spoke with a gentleman who'd bought a £119k Maserati, discounted to £105k. 8-weeks later with very few miles on the clock it was involved in an accident and written off. There were only three of the cars in the UK at the time, only one of which was on sale, with slightly higher mileage than his car but for virtually the full list price of £119k. His insurer (despite being one that does NOT provide New-For-Old cover) paid out the full list price of £119k - no claim required of his GAP insurance policy! It would be a different matter of course, if say, you had a claim after 6-months because at that point a "gap" has of course formed. So let's look at that using a hypothetical example and some of your figures from above: [a] Car purchased for £23,000 Borrowed £16,000 [c] Written off @ 6-months old, Motor Insurer pays £19,000 [d] Balance outstanding on finance @ 6-months = £14,500 (assuming 0% and repayments of £250 per month) [e] List Price for replacement car @ time of claim £25,000 Replacement GAP insurance would pay the £6,000 difference between your Motor Insurance payout [c] and the £25,000 cost of replacing the vehicle brand new [e]. You'd then settle [d] the £14,500 outstanding on finance and you'd have £10,500 left over to put towards the cost of your next car and as mentioned above, unlike some other GAP insurance providers, we don't apply any restrictions as to what vehicle you buy or from which motor dealer. As for the Service Plan, unlike GAP insurance policies of old, we no longer specifically exclude the cost of the service plans etc from a payout, however it would only become a consideration initially on a pro-rata basis (the amount of unused cover that remains at the time of claim) and only then if the outstanding balance was not available for you to reclaim and/or transfer forward against a new car. Defaqto. A company has to purchase a licence from Defaqto in order to display their star-rating on their website and documentation etc. When (after discovering the Defaqto GAP insurance review and pointing out errors they'd made in the facts about our policies) I initially enquired as to the cost of such a licence I was quoted circa £13,000! After I'd picked myself up and got my bearings, the guy I was corresponding with claimed he'd made a mistake and revised his quote but it was still a substantial figure and by that time I'd switched off. I'm pretty sure he'd have taken £13k off us if I'd have agreed to it. It's very nice of Defaqto to have rated our policies as highly as they have (without a licence I'm not permitted to state how highly) but I'm/we're not prepared to pay the sums they asked for in order to have the privilege of being able promote their rating. Besides, IMO their rating criteria has (seemingly under pressure) been skewed more recently in favour of getting more companies (namely Motor Dealers) the coveted 5-star rating (more companies shouting about their ratings = more money for Defaqto) when in fact there are considerable albeit sometimes intricate differences between many of the 5-star rated policies that should warrant a 6-star rating being created - of which IMO we would be worthy! :p If you (or anyone else) has any other questions, don't hesitate to ask.

-

Hi Andrew, If your Motor Insurer covers New-For-Old in the first year and having checked how it works and what conditions apply to it etc, you're happy to defer the start date of your GAP insurance policy by the first year, you could purchase a 3-year policy and delay it by up to 12 months from when the vehicle was first registered. Technically if you delayed by the whole year this would leave your 3-year policy covering years 2, 3 and 4. If you sold your vehicle at 42 months subject to how the dates fall there'd be 6-months cover remaining on your GAP insurance policy. You'd cancel it, claim a rebate of the unused premium (the value of those 6-months) and then use that sum against the cost of a new policy on a new vehicle. No cancellation or transfer fee would apply. In terms of the Claim Limit, there's a few ways you can approach this and I'd need to know a little more about your finance agreement, your car and how many miles per year you're going to drive in order to advise you more accurately, however, the general rule of thumb is that the average car is expected to depreciate by between 50% and 70% over a three year period. To this end, I wouldn't recommend taking a claim limit of any less than 50% of the original purchase price but in your case with a policy potentially covering in to the 4th year I'd be leaning closer to the 70% mark. Note that if you're considering Replacement GAP insurance, it's normal to take a higher Claim Limit than you would with an Invoice GAP insurance policy because unlike Invoice GAP insurance when all you're primarily concerned about is by how much the car will drop in value from the price you paid first time, with Replacement GAP insurance there's also the potential for the list price for the brand new vehicle cost to increase too. Another good way to get a starting point for your Claim Limit is that if you have a PCP agreement you can approach the Claim Limit as follows: Invoice GAP Insurance - Deduct the guaranteed future value of the vehicle (the final repayment under the PCP agreement) from the original cash price (after discounts) you paid for the vehicle. Replacement GAP insurance - Deduct the guaranteed future value of the vehicle from today's list price (before discounts) for the brand new vehicle Using this "PCP" approach, your Claim Limit should not be less than the resulting figure... how much higher you take it is your own personal preference. In terms of the forum-discount, you'll need to buy your GAP insurance policy over the phone, or get in touch with me via DM or email to furnish me with all the details and I can create a discounted policy on our online system for you to simply log in to, retrieve and pay for.